After back-to-back annual returns like this, why do I think these stocks will outperform again?

It’s simple: They’re incredible companies. They have massive scale, competitive moats, and huge competitive advantages.

There’s a reason why they’ve performed so well over the past couple of years, and I think they can do it again.

Now, I know many people out there will disagree. So it will be a big surprise if things go how I anticipate.

Perhaps more surprisingly, I believe that the market’s favorite stock, Nvidia (NVDA), will lag in 2025.

That’s because we’re moving from the network-building phase of the AI boom to the implementation and harvesting phase. So investment will shift from hardware to software.

The shift could set Nvidia up for disappointment, especially after two tremendous years that have set extremely high expectations.

On the other side, companies that have spent money on building the network — Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG), and Meta Platforms (META) — will see their capital expenditures lessen.

This could lead to an explosion in earnings and cash flow at these companies, powering the Mag 7 to greater heights while leaving Nvidia behind.

2: Small-Caps Will Continue to Struggle

The second most popular prediction for 2025 (after Mag 7 underperformance) is that small-cap stocks will finally start to pull ahead of the large-caps. Again, I disagree.

There are particularly good reasons why small caps have underperformed over the last few years, and those won’t change in 2025.

These are sub-scale companies with inferior balance sheets and more exposure to macroeconomic variables like inflation, interest rates, and commodities.

This doesn’t mean small caps will go down in 2025. I just doubt they will keep up with their larger brethren.

Sometimes, stocks are cheap for a reason. That reason will not change anytime soon for small-cap stocks.

3: Interest Rates and Inflation Won’t Matter

After two years of dominating the headlines and creating volatility, I think that movements in interest rates and inflation won’t matter much to the stock market this year.

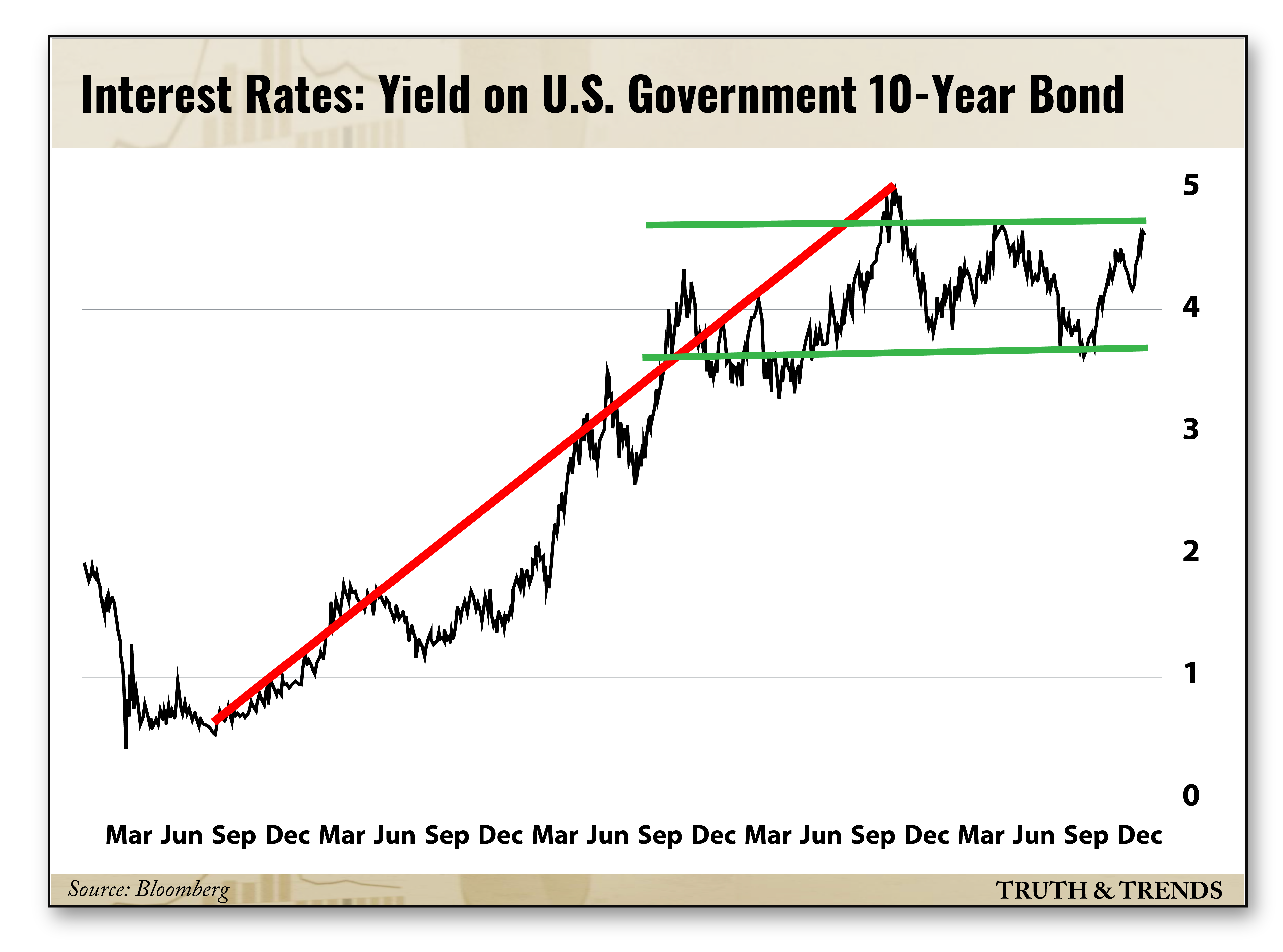

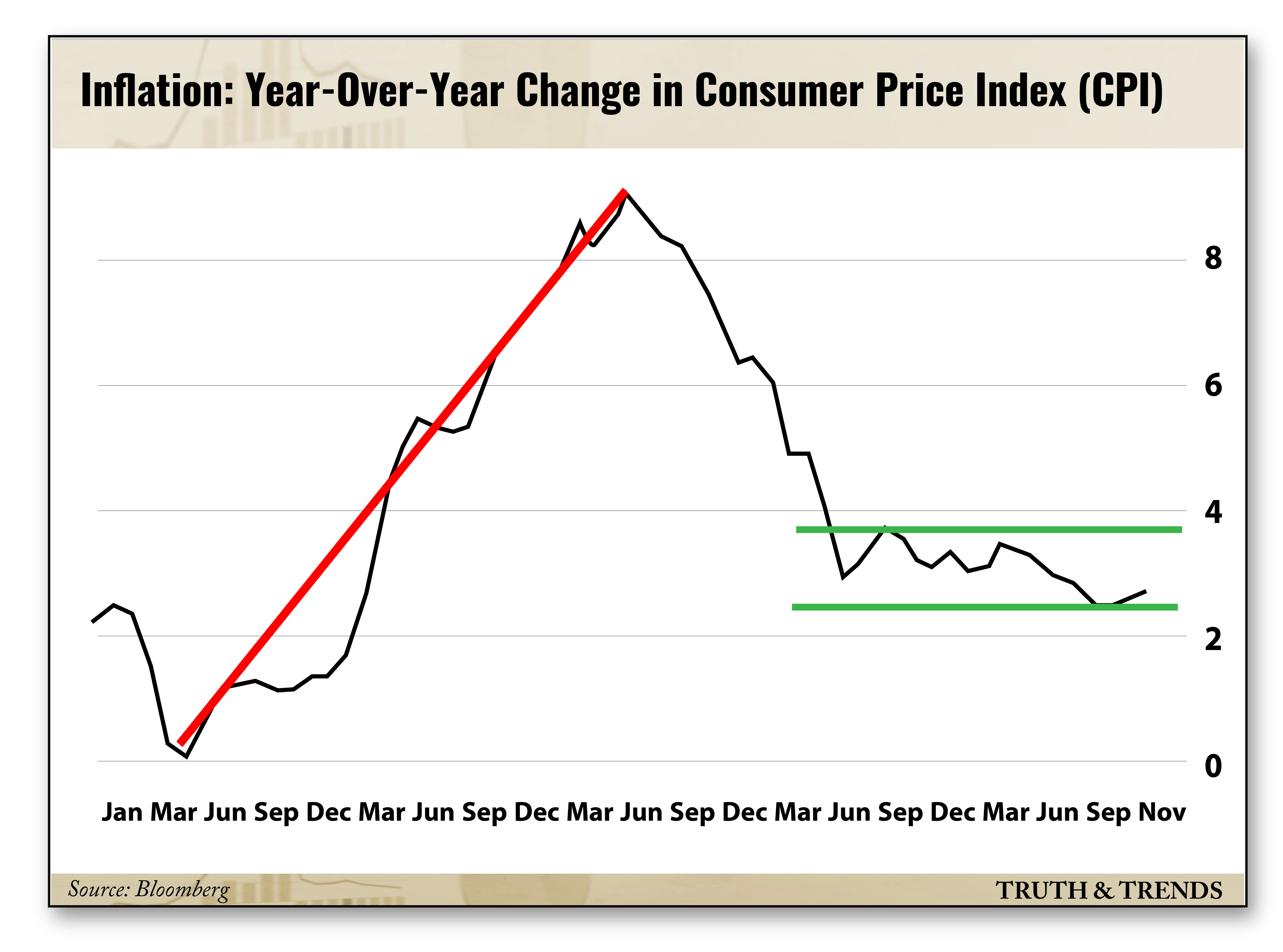

The reason these variables had so much influence in the last few years is that we were quickly going from exceptionally low levels in each to much higher levels (highlighted by a red line in the following charts).

Here’s a chart of the U.S. 10-year Yield…

No comments:

Post a Comment

Keep a civil tongue.