June 24, 2024 | Read Online | | Value Investor Daily #35 Toll Brothers (TOL) - Luxury Homebuilder With a Stock That Looks Cheap |

| | | In partnership with |  |

| With Deal Sheet you get curated, actively investable startup opportunities sent once per week. | | Deal Sheet offers the best (and actively investable) venture capital investment opportunities directly to your inbox weekly. Deal Sheet subscribers have already received investment opportunities alongside Kleiner Perkins, Naval Ravikant, General Catalyst, Andreessen Horowitz, Khosla Ventures and more! | The Deal Sheet Co-Founders Alex Pattis and Zach Ginsburg are the global VC Syndicate leaders with over 700 investments closed and over $200m invested into startups. Additionally, over the last five years, Alex & Zach have collaborated on deals with over 50 VC leads who have collectively put together well over 1,000 startup investments. | Sign Up Now | | Toll Brothers, Inc. (NYSE: TOL) stock is up more than 14% year-to-date, yet with a P/E ratio (TTM) of just 8.04, it still appears cheap. Is it undervalued? | Company Profile | Toll Brothers designs, constructs, markets, and sells luxury detached and attached homes in residential communities throughout the United States. | Aimed at affluent buyers, the company provides large, high-end residences that cater to a niche market. | This strategic emphasis on the luxury segment sets Toll Brothers apart from its biggest competitors, enabling it to capitalize on the demand for upscale living experiences. | Financial Performance | Toll Brothers has been maneuvering through a challenging market landscape that includes changing consumer preferences, economic uncertainties, and competitive pressures. | The company is highly sensitive to macroeconomic factors like interest rates and tax policies, which can affect buyer affordability and sales. | Moreover, its relatively high average selling prices (ASPs) compared to competitors could present challenges in less favorable economic conditions. | Despite these challenges, Toll Brothers has beaten EPS and revenue consensus estimates for the last seven quarters. | Revenue is expected to grow by 5.39% in fiscal 2024, 2.68% in 2025, and 6.12% in 2026. | Diluted EPS, excluding extraordinary items, is projected to grow by 14.09% in 2024, 0.47% in 2025, and 9.84% in 2026. |  | Source: Capital IQ |

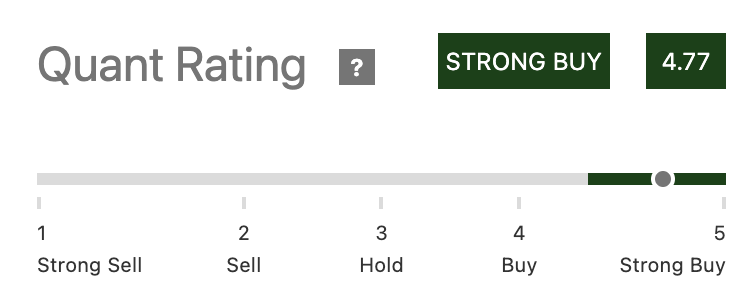

| The company's return on equity (ROE) has improved significantly from 11.9% in 2019 to 23.0% over the last twelve months (LTM). | Recent Earnings | On May 21, Toll Brothers announced Q2 results that surpassed expectations in deliveries, margins, and other income. | The company reached a record home sales revenue of $2.65 billion, a 6% increase compared to the previous year. | Furthermore, the company experienced a significant 30% year-over-year growth in orders, twice the analysts' projected 15% increase. | Toll Brothers has shown resilience despite elevated mortgage rates, successfully tapping into the strong demand for homes that continues to exceed supply. | Contrary to initial expectations, the company has maintained a solid sales trajectory, selling more high-end homes than anticipated. | The market's prediction that consumers would delay purchases until mortgage rates declined has not come to pass. | The company has increased its full-year guidance, expecting revenues of $10.23 billion from the delivery of approximately 10,600 homes at an average price of $965,000. | Key success factors include a wider range of price points, an increased supply of spec homes, and strong cost controls, achieving an adjusted gross margin of 28.2% for the quarter. | Despite the strong quarterly performance, Toll Brothers' shares have declined since the latest earnings announcement due to investor concerns over a projected dip in gross margin from the mix of speculative homes sold. | Nevertheless, analysts view the overall trends for Toll Brothers as positive. | Our Take | We remain positive about Toll Brothers' dominant position in the luxury market, anticipating that the housing sector will benefit from favorable demographics and years of underproduction. | Toll Brothers continues to prioritize maintaining a strong balance sheet and increasing production. | The company's strategic initiatives are focused on growth and efficiency improvements, which could enhance its market position. | However, industry-wide challenges and capital constraints could affect these expansion plans. | If the Federal Reserve lowers rates, demand for Toll Brothers homes and ASPs will likely increase, causing a reset in revenue projections—but only if a recession is not in play. | Valuation and Analyst Sentiment | Our fair value calculation, using 13 valuation models including Earnings Power Value, EV/Revenue Multiples, P/E Multiples, and 10Y DCF EBITDA Exit, estimates the company's fair value at approximately $142, suggesting a potential upside of nearly 21% from the current stock price. | According to Seeking Alpha's quant rating, the company receives a Strong Buy rating, considering factors such as valuation, growth, profitability, momentum, and revisions. |  | Source: Seeking Alpha |

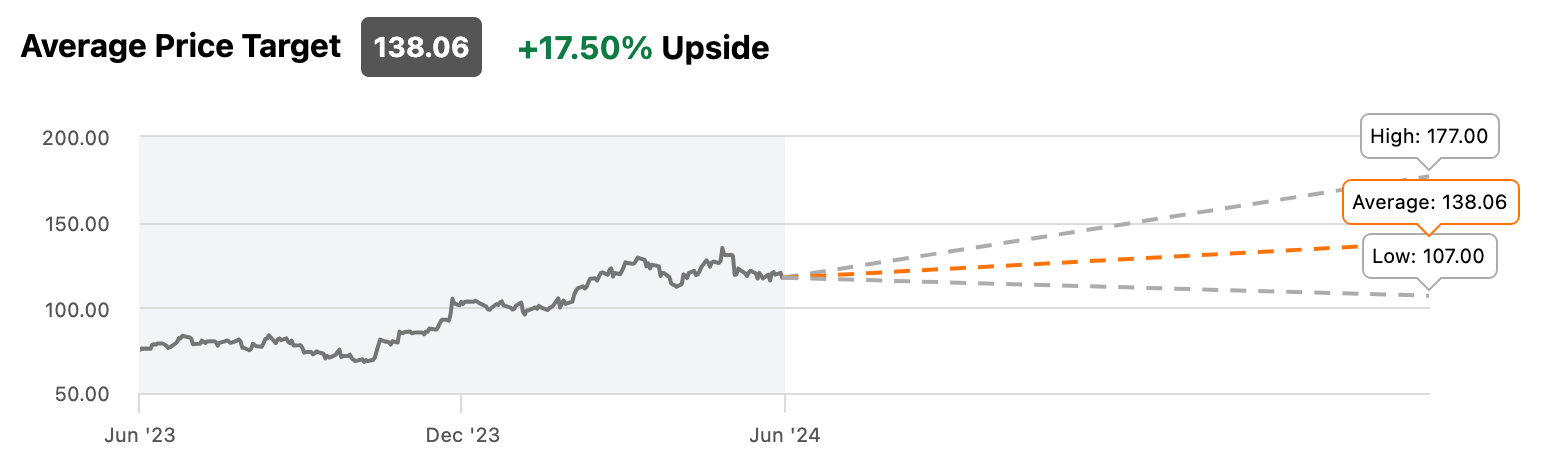

| Wall Street analysts are also bullish on Toll Brothers, maintaining an average Buy rating with price targets ranging from $107 to $177, and an average of $138.06, indicating a potential upside of 17.5% from the current stock price. |  | Source: Seeking Alpha |

| Expect management to take advantage of the current valuation by repurchasing shares. | Since 2014, the company has bought back over 40% of the diluted shares outstanding and was authorized in December 2023 to buy back another 20 million shares (vs. 111 million outstanding at year-end 2023). | On the last earnings call, Chairman and CEO Douglas Yearley said they plan to continue the shareholder return program indefinitely: | During the quarter, we repurchased $181 million of common stock and increased our quarterly dividend by 10%. Returning cash to stockholders will continue to be a very important part of our strategy well into the future. |

|

| Conclusion | Given its fair value estimate, solid financial position, and future opportunities, Toll Brothers' current valuation is appealing. | We believe the stock is currently undervalued, making it an attractive hold. If the stock price falls to $92.30, a margin of safety of 35%, it would move to a strong buy. | Do your own research and decide. Thank you for reading today! | | | | |

| | | | | Copyright © 2024 Value Investor Daily, Kaizen Media, LLC. 11801 Domain Blvd 3rd floor, Austin, TX 78758. All rights reserved. No part of this newsletter may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law | Comprehensive Disclaimer: The content in this newsletter is strictly for educational and informational purposes. It is not, in any circumstance, intended as financial, investment, legal, or tax advice. The author and publisher of this newsletter are not licensed financial advisors, certified public accountants, or legal professionals. | While every effort has been made to provide accurate and up-to-date information, there is no guarantee that such information is free from errors, inaccuracies, or omissions. Investing, trading, or applying any of the strategies discussed herein carries inherent risks, and you should not rely solely on this information to make any financial decisions. | All forecasts, market viewpoints, calculations, and estimates published here are forward-looking statements and are therefore intrinsically unpredictable. Predictions are only forecasts constructed with educated assumptions and are not correlated whatsoever to future circumstances that may or may not happen in reality. Unforeseen events may impact returns or performance of securities discussed in this document. The information provided is current as of the preparation date and may not reflect future developments. Publisher is not obligated to update or revise this information. Readers should exercise judgment when making investment decisions based on this document. | Publisher and its associates may hold or acquire long or short positions in mentioned companies' securities, which may result in financial gain or loss. However, there is no guarantee that these positions will be maintained. | The publisher and its affiliates are not liable for any direct or consequential loss arising from the use of this information. The information provided is for informational purposes only and should not be considered a substitute for professional advice. The user is responsible for evaluating the accuracy, completeness, and usefulness of the information provided. The publisher and its affiliates do not endorse any products or services mentioned in this document. | This newsletter may contain links to third-party websites or resources. The author and publisher have no control over, and assume no responsibility for, the content, policies, or practices of any third-party websites. | To the fullest extent permitted by law, the author and publisher disclaim all liability for any loss, damage, risk, or consequence, whether direct, indirect, or consequential, faced by any person who directly or indirectly relies on the information provided in this newsletter. | You should consult with a qualified financial, legal, or tax professional before taking any action based on the content of this newsletter. | Affiliate & Sponsored Links Disclaimer: This newsletter may contain affiliate links or sponsored content. This means that if you click on one of these links and make a purchase or engage with the website, Publisher may receive a commission or benefit in some way. The inclusion of any links does not necessarily imply a recommendation or endorsement of the views expressed within them. | | | Update your email preferences or unsubscribe here © 2024 Value Investor Daily, Kaizen Media, LLC. 11801 Domain Blvd 3rd floor, Austin, TX 78758 228 Park Ave S, #29976, New York, New York 10003, United States | |

|

|

|

|

|

No comments:

Post a Comment

Keep a civil tongue.