Editor’s Note: Warren Buffett has never been afraid to sit on the sidelines when markets look frothy. But with Berkshire Hathaway now holding a record $325 billion in cash, some investors are starting to ask: is he being cautious… or missing something big?

In this Sunday Spotlight, Sean Ring of The Morning Reckoning looks at one asset Buffett has turned to before — and why his successors might make the call that he won’t.

The Sunday Spotlight: Buffett's $325 Billion Mistake

|

| SEAN

RING |

Hi Reader,

Warren Buffett, the Oracle of Omaha, is facing a peculiar problem these days: he has too much cash.

Berkshire Hathaway is sitting on an eye-watering $325 billion in dry powder, a record high. Historically, Buffett has always been eager to deploy capital when the odds are in his favor. But today, even he admits he’s struggling to find value in this overvalued market.

Which leads to a fascinating question: could Buffett turn to silver, or even silver miners, as a way to put that cash to work?

To answer that, let’s take a short trip back to the late 1990s when Buffett made one of his more unconventional moves.

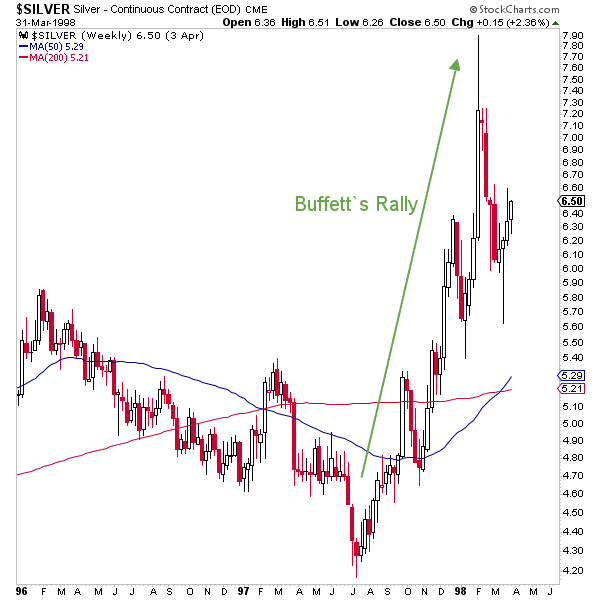

Buffett’s Big Silver Bet in the 1990s

In 1997 and 1998, through Berkshire Hathaway’s General Re subsidiary, Buffett bought about 130 million ounces of physical silver. That’s roughly 20% of the world’s known above-ground supply at the time.

His rationale was Classic Buffett: supply and demand.

Silver had been beaten down for years, with central banks selling their reserves and industrial demand remaining relatively stable. Buffett saw the price, around $4.40 per ounce, as disconnected from the underlying fundamentals.

Buffett’s mentor Benjamin Graham once told him, “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

He figured silver’s actual value would eventually be “weighed” and the price would rise accordingly.

Of course, Buffett was right. Silver prices did move higher, peaking around $7 per ounce in the late 90s. Depending on the price Buffett closed the trade, he made anywhere from $208 million to $328 million.

However, the trade attracted regulatory scrutiny. The CFTC investigated whether Buffett had cornered the market. While they found no wrongdoing, the experience likely left Buffett with a bad taste in his mouth.

How 1998 Relates to 2025

Today, silver finds itself in a similar situation.

Industrial demand for silver is surging, especially for solar panels, electric vehicles, and advanced electronics. Yet mine supply is struggling to keep up. Add in a general underinvestment in new mining projects, and you’ve got a classic supply-demand imbalance brewing.

Meanwhile, institutional ownership of silver remains very low. Hedge funds, pension funds, and endowments aren’t piling into silver the way they are with equities or even gold.

In short, the fundamentals look tight, and the market doesn’t fully reflect that yet, just like in the late 1990s.

No comments:

Post a Comment

Keep a civil tongue.